Rwanda Broadcasting Agency | Businesswomen call for streamlined means of access to finance and investment opportunities

Rwanda Broadcasting Agency

Businesswomen call for streamlined means of access to finance and investment opportunities

By tailoring content and digital targeting, SME Response Clinic is actively equalizing the information asymmetry that prevents women entrepreneurs from safely accessing finance and training. ConsumerCentriX is proud to serve as the implementing partner in this critical initiative.

Nothing found.

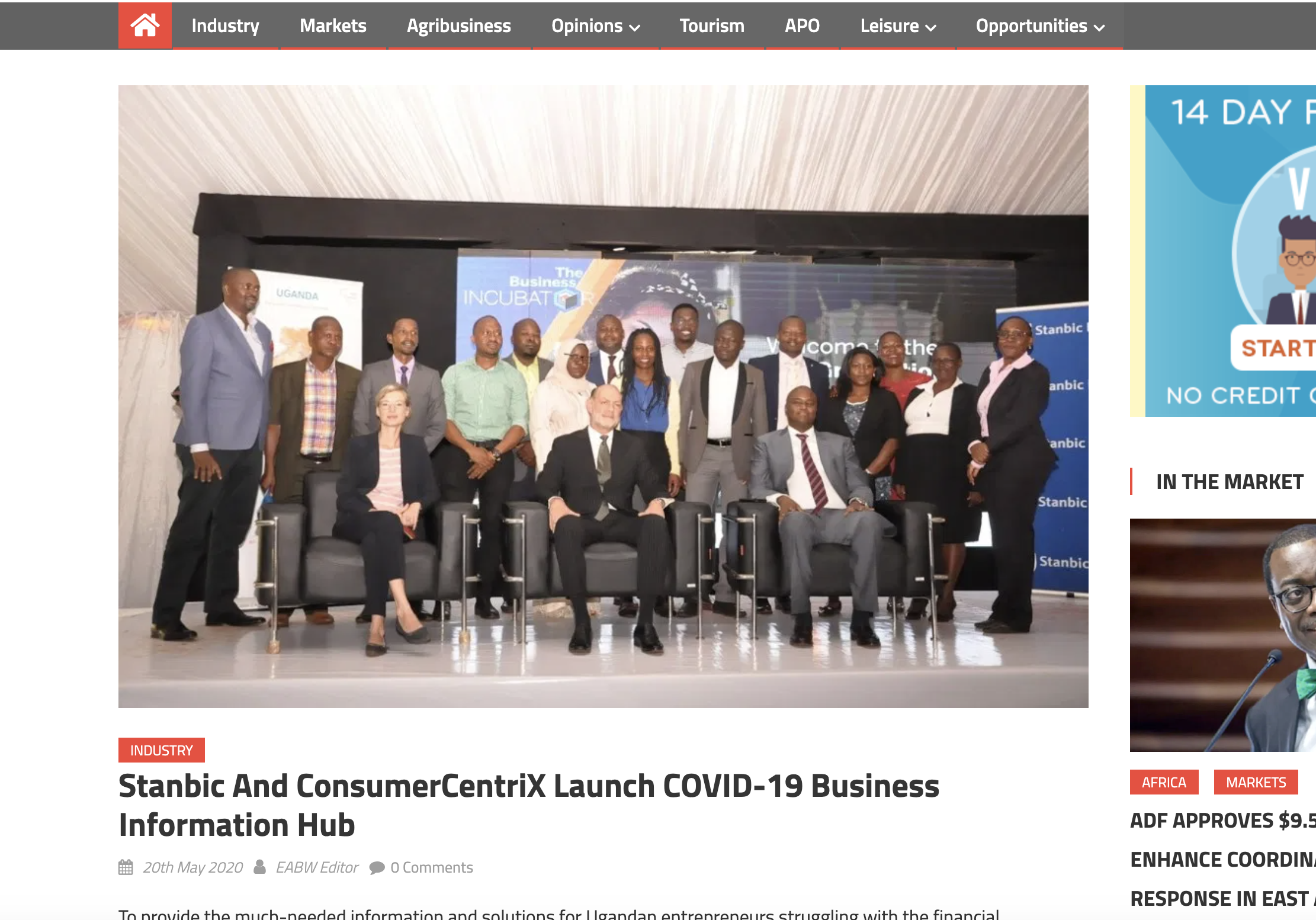

EABW NEWS | Stanbic And ConsumerCentriX Launch COVID-19 Business Information Hub

Stanbic And ConsumerCentriX Launch COVID-19 Business Information Hub

To provide the much-needed information and solutions for Ugandan entrepreneurs struggling with the financial consequences of the COVID -19 pandemic, Stanbic Bank has partnered with ConsumerCentriX on a Business Information Hub.

This website will provide entrepreneurs with advice on financial management to overcome economic slowdown and insights into new developments across industries.

Through a partnership with the African Management Institute (AMI), the Covid-19 Business Info Hub will promote informative virtual training sessions and webinars to help entrepreneurs navigate these challenging new circumstances.

Employing over 2.5 million people, small and medium enterprises (SMEs) are the key driver of growth for Uganda’s economy.

Rwandan Online Business Bootcamp Launched

Rwandan Online Business Bootcamp Launched

By Alejandra Ríos and Jessica Massie

A version of this article was originally posted on the SME Response Clinic

To support entrepreneurs in these challenging and unprecedented times, Access to Finance Rwanda (AFR) has partnered with the Rwanda Private Sector Federation and ConsumerCentriX on the SME Response Clinic. This digital platform provides entrepreneurs in Rwanda with information on financial management and industry insights to improve their response to this crisis.

However, information alone is not enough. As a result of this conviction, the SME Response Clinic is promoting a series of webinars and virtual programs through a partnership with the African Management Institute (AMI), to help entrepreneurs to adjust to financial uncertainty by deepening their skills and business acumen.

On Tuesday, May 12th, small businesses in Rwanda across sectors and with different business sizes joined the first FREE “Business Survival Bootcamp” facilitated by the African Management Institute (AMI).

Jean Bosco Iyacu of Access to Finance Rwanda (AFR), opened the webinar with a message of solidarity for the SME Response Clinic and SMEs in Rwanda.

The webinar takes businesses through important tools for planning during the COVID-19 pandemic.

These include:

- Scenario planning for your business – how do you deal with issues regarding customers, suppliers, infrastructure, staff and cash flow? How will these be affected if I close or have slow business for two weeks? What if it is two months?

- Organizational risk assessments – looking at the different dimensions of business, the risks they face, and how to mitigate them. What do you do if you can’t get the goods you need for your store, or supply your customers?

- Impact on cash flow – what to do if and when your cash flow is affected by an unexpected closure or low period.

All participants are given access to tools, such as cash flow planning spreadsheets, from AMI to use to help in their own businesses. These resources are free and designed specifically to navigate the issues in the COVID-19 pandemic, and include additional courses.

These tools and conversations are important given that the pandemic is likely to continue to affect SMEs in Rwanda – and around the world – for an unknown period of time. According to Diederik Wokke of AMI, many small businesses originally thought they would be affected for just the first two weeks of the lockdown. Now that the situation is stabilizing but slowly, businesses still need to build these skills and plan for a more uncertain future.

Conversation during the training highlighted some of the questions that SMEs have right now. For example, supplier negotiation is becoming more difficult now that businesses are able to open little by little. A shop renting a space may have had more flexibility in terms of payment during the lockdown, but this is changing as the country opens.

Finally, there are still many questions around payments and transferring to contactless mechanisms as much as possible. Many businesses are switching to digital payments and are still in the learning phase.

But with planning, management, and resources like those available from the SME Response Clinic, small businesses will be more likely to survive this pandemic.

Find out more about the upcoming sessions at “Expanding My Skills” on the SME Response Clinic website and on Facebook.

About the Authors

Alejandra Rios is an expert in inclusive finance with a focus on small-and-medium (SME) enterprises, advising leading commercial banks and microfinance institutions in emerging markets for the past twenty years. Her portfolio in MSME finance consultancy covers change management, housing finance, rural finance, institution-building, strategic planning, and credit management. She is a Partner at ConsumerCentriX.

Jessica Massie is a consultant in financial capability and microfinance based in Kigali, Rwanda. She has lived and worked in a variety of African countries for almost 20 years, and specializes in curriculum development, training, research and writing, with a focus on skill-building and behavior change. She is working with the ConsumerCentriX team on the SME Response Clinic in Rwanda.

RELEVANT NEWS & INSIGHTS

All Africa | Rwanda: COVID-19 - Private Sector Inks Deal to Support SMEs

All Africa | Rwanda: COVID-19 - Private Sector Inks Deal to Support SMEs

The Private Sector Federation on Monday, May 4, signed a Memorandum of Understanding with Access to Finance Rwanda in a new initiative aimed at supporting entrepreneurs in Rwanda to adjust to economic realities of COVID-19. The parties to the deal, as noted, seek to share their respective strengths, experiences, technologies, including technical assistance to facilitate Small and Medium Enterprises (SMEs) during the COVID-19 pandemic. They also seek to collectively support businesses in the short, medium, and long term.

Find more about SMEs support here.

Stanbic Uganda in partnership with ConsumerCentriX launch the COVID-19 Business Information Hub

“ConsumerCentriX is honored to continue working with Stanbic Bank on further strengthening its small and medium enterprise proposition to address these challenging times. Being relevant, providing support promptly can make the difference for enterprises today,”

-ANNA GINCHERMAN,PARTNER AT CONSUMERCENTRIX.

To provide the much-needed information and solutions for Ugandan entrepreneurs struggling with the financial consequences of the pandemic, Stanbic Bank has partnered with ConsumerCentriX on the Covid-19 Business Info Hub.

This website will provide entrepreneurs advice on financial management to overcome economic slowdown and insights into new developments across industries. Through a partnership with the African Management Institute (AMI), the Covid-19 Business Info Hub will promote informative virtual training sessions and webinars to help entrepreneurs navigate these challenging new circumstances.

Employing over 2.5 million people, small and medium enterprises (SMEs) are the key driver of growth for Uganda’s economy. However, as the COVID 19 pandemic unfolds, the SME sector faces reduced business activity and financial security as a result of disruptions to the supply chain, travel restrictions, and changing work environments.

Over the last few months, Stanbic Bank has already introduced a range of innovative products and services to support entrepreneurs with overcoming these challenges. For example, to address reduced revenues and cash flow, clients can now access an unsecured overdraft facility within 24 hours based on the performance of their banking history. To reduce disruptions in the supply chain, the bank has partnered with Zhejiang International Trading Supply Chain Co Ltd to support enterprise clients importing from China.

The Covid-19 Business Info Hub will become a centralized platform for Stanbic to communicate these responsive efforts with enterprise clients in Uganda. However, the vision of the site is to become a trusted resource for all entrepreneurs in Uganda, looking for industry insights and relevant virtual training sessions.

“We are aware of various the challenges businesses are facing especially during this time, and we are committed to unlocking new solutions to enable business continuity. Among the key initiatives, Stanbic has put in place to support businesses is the loan repayment holidays, as a measure to protect clients from adverse economic effects of the COVID-19 pandemic. We will also continue to be at the forefront of delivering wholesome solutions to entrepreneurs directly through strategic alliances and partnerships to keep them thriving during and post the pandemic,” said Grace Muliisa, Stanbic Uganda’s Head of Personal and Business Banking

As the implementing partner, ConsumerCentriX is well-positioned to support Stanbic Bank’s on this critical endeavor. ConsumerCentriX is an international strategy consulting firm that works with financial service providers and policymakers on translating consumer insights into market strategies and policies to reach the un/undeserved. The firm has extensive experience supporting SME development in East Africa through financial and non-financial services.

“ConsumerCentriX is honored to continue working with Stanbic Bank on further strengthening its small and medium enterprise proposition to address these challenging times. Being relevant, providing support promptly can make the difference for enterprises today,” said Anna Gincherman, Partner at ConsumerCentriX.

Visit the Covid-19 Business Info Hub

RELEVANT NEWS & INSIGHTS

Introducing the SME Response Clinic

The Private Sector Federation, Access to Finance Rwanda and ConsumerCentriX in a Joint Covid-19 Response Partnership for Support to Rwanda’s Medium, Small and Micro Enterprises.

READ THE OFFICAL STATEMENT TO THE PRESS

Kigali – 5th May 2020: To support entrepreneurs in Rwanda struggling to adjust to the economic realities of Covid-19, the Rwanda Private Sector Federation has partnered with Access to Finance Rwanda (AFR) and ConsumerCentriX on the SME Response Clinic. This digital platform will translate new policies and financial advice using a clear and straightforward language in both English and Kinyarwanda.

With 148,092 MSMEs in Rwanda representing 99.7 percent of the businesses according to the Integrated Business Enterprise Survey (2017) by the National Institute of Statistics of Rwanda (NISR), this sector plays a pivotal role in the country’s socio-economic development.

However, getting access to the right information, training, and finance is no easy feat. Even before the crisis, a number of studies, including ConsumerCentriX’s research in May 2019 and Private Sector Federation’s Business and Climate Survey April 2019 respectively indicate MSME owners face several critical challenges even at the time of economic growth and stability.

The consequences of COVID-19 pandemic further exacerbate challenges faced by MSMEs by significantly reducing their business activities and financial security. The Rwandan government and financial sector have taken several significant measures to support MSMEs during this challenging period. To ensure that these important measures are communicated to MSMEs in an accessible and timely manner, the Private Sector Federation in partnership with Access to Finance Rwanda and ConsumerCentriX developed the SME Response Clinic, a digital platform that translates relevant policies and financial advice to the SMEs.

For high quality and relevant content, interviews will be regularly conducted with financial service providers, industry experts, policymakers, and MSMEs. All information will be centralized on the SME Response Clinic website and promoted through SMS, social media campaigns, and different media channels.

“Being the catalyst of a deeper and inclusive financial sector in Rwanda, Access to Finance Rwanda sees the MSME Response Clinic as a key tool in addressing information asymmetry between policymakers, Financial Services Providers and the MSMEs. It also provides an opportunity to understand the real needs of SMEs so as to be able to effectively support them during this unprecedented crisis of Covid-19” said Waringa Kibe, AFR Country Director.

Ms. Anna Gincherman, Partner of ConsumerCentriX believes that if well implemented, the new partnership will yield positive results for the Country’s private sector. “As the leading implementing agency for this project, ConsumerCentriX is well-positioned to accomplish the project objectives due to its extensive background in SME development in Sub-Saharan Africa, including Rwanda, its expertise in working with financial service providers and regulators, and its in-house capacity to manage digital communication,” she added.

Meanwhile, The Private Sector Federation Chief Executive officer Mr. Stephen Ruzibiza commended the new partnership adding that it has come at the right time when MSMEs need strong recovery approaches in terms of various aspects including to the right information and access to finance.

“We welcome this partnership as the SME Response Clinic will provide and collect needed information that will enable key stakeholders to support the resilience of the MSME Sector in this period of Covid-19, ” said Mr. Ruzibiza.

Through a partnership with the African Management Institute (AMI), the SME Response Clinic will be promoting a series of webinars and virtual programs to help entrepreneurs adjust to new realities and ensure resiliency for the future.

For more information, please contact.

Musa Kacheche

Communication & Media Lead

ConsumerCentriX

Email: musa.kacheche@consumercentrix.ch

New ways to train businesses on a growth path with Rebecca Harrison

REACHING THE UNDERSERVED: EPISODE 3

New ways to train businesses on a growth path with Rebecca Harrison

If you can get entrepreneurs and their teams to implement some simple but effective habits, then you very quickly start to see results

-REBECCA HARRISON

Co-Founder and CEO, African Mangaement Institute (AMI)

Wanjiru Mbugua [00:00:00] I had this idea but had not started, RD clothing. And so when we started on the second month of my training, I remember there’s this trainer who asked us, what do you think are your four best ideas, business ideas that you can work with from the comfort of your bed? You know, something that people would be using, something that people don’t like, something unique, something interesting that you would do as a business and change your life and change other people’s lives. I said “That’s it.” That’s it for me. That was it. That’s all I needed.

Narration [00:00:48] The African Management Institute, commonly known as AMI, has developed Africa’s first scalable solution for skills and enterprise development. Their blended methodology focuses on encouraging adoption of effective business practices. It does this by combining web and mobile platforms with in-person workshops to help participating entrepreneurs develop the skills and habits they need to grow their businesses. Two years ago, AMI expanded its impact in this space by partnering with Kenya Commercial Bank, one of the largest retail banks in East Africa. Through this partnership, KCB’s business clients were invited to join AMI’s Grow Your Business program. Anna Gincherman, Partner at ConsumerCentriX sat down with Rebecca Harrison, co-founder and CEO of AMI to learn more about how blended learning works, how it addresses different profiles of entrepreneurs, particularly women, how it benefits partner banks, and how results are being measured.

Anna Gincherman [00:01:53] Rebecca, you can start with you introducing yourself and just a few words about AMI?

Rebecca Harrison [00:02:01] My name’s Rebecca Harrison. I’m the co-founder and CEO of AMI, African Management Institute and we enable ambitious businesses across Africa to thrive. We do that through practical tools and training. AMI has been around for about five or six years. We have offices in Nairobi, Kenya, Jo’burg in South Africa and Kigali in Rwanda. We’ve trained about 27,000 people, managers, leaders, entrepreneurs and their employees in about 15 countries across Africa.

Anna Gincherman [00:02:30] The ConsumerCentriX team spent about a week in Nairobi talking to clients of KCB Bank, learning about their experience with the bank’s financial and non-financial services. And many of the clients were raving above the program. They took in 2017, which was conducted by AMI and my favorite quote from the primary school entrepreneur, Simon, was his name, was “these people (meaning KCB and AMI) don’t even know how good this program is and how important it was for us.” So very positive feedback. So it would be great if you can describe what this magic program is, what’s different from what else is out there and why you think it was so influential?

Rebecca Harrison [00:03:22] I’m delighted to hear entrepreneurs are saying good things about us. So, Grow Your Business is a whole new approach to learning for entrepreneurs. So I guess what we’ve done at AMI, is to turn training on its heads. What traditional training does has take entrepreneurs out of their business and put them in a classroom and has an expert talk at them. And what we see, in terms of results, is that entrepreneurs really struggle to translate that kind of knowledge into any real change in the business. They might get some new knowledge, but then that doesn’t really translates into any kind of real result for the business. So what we’ve done at AMI, is we’ve really dug into the evidence base and the research around what works in developing SMEs and entrepreneurs.

And the big insight and the secret sauce of Grow Your Business is that what makes the difference for is business practices and habits. And if you can get entrepreneurs and their teams to implement some simple but effective habits, then you very quickly start to see results. So when we were designing Grow Your Business, we were thinking both about, you know, how can we really drive impact, but how can we do that in a way that’s cost-effective. And that’s where we came up with this blended model. And the idea of blended learning is that you combine online tools and resources. We provide those through a mobile app as well as an online platform. And the idea is that our entrepreneurs can access practical tools online, anytime, anywhere, and you can apply them immediately in the business. So we’re not taking entrepreneurs out of the business for days on end. We’re going to them at that point of need. So that’s the first piece is the online tools.

The second piece we’ve learned in an African context, purely online learning doesn’t really work on its own. So you still need some kind of human components, kind of human touch, as it were. We combine the online tools with experiential in-person Face-To-Face workshops. But we don’t do as many of the traditional programs. So, again, we’re not taking people out of their businesses for days on end. Over a course of six months, we take the entrepreneurs out for three days, beginning, middle and end. And they have really high impact experiences. So those are really memorable days. You know, they’re not sitting listening to someone talk. They’re interacting, they’re networking, they’re role-playing and practicing some of these tools that they’ve been downloading on their phones and on their computers and getting a feel for what does that mean for me and my business? Blended learning often only really covers those two components online and in-person. We take it a step further and when we say, well, it’s online tools, in-person experiences and then in the business or on the job practice and application. Throughout our program, we’re journeying with our entrepreneurs to support them and incentivize them to implement these habits and practices in the business.

At the office of African Managment Institute in Nairobi, Kenya

In terms of gender, we’ve seen some really interesting trends. So we noticed on the program with KCB, for example, at the intake level, there were, I believe, it’s 55 percent men and 45 percent women. When we looked at the completing entrepreneurs, that ratio had flipped. So 55 percent of the competing entrepreneurs were women and 45 percent were men.

-REBECCA HARRISON

Co-Founder and CEO, African Mangaement Institute (AMI)

Anna Gincherman [00:06:24] Excellent. And do you think this approach fits best, a particular profile of an entrepreneur? We know the SME segment is heterogenous as there are so many different types of business, sizes of businesses, and there is a gender aspect to it. Do you think your program is best suited for a particular profile or it’s kind of a universal application?

Rebecca Harrison [00:06:47] Yeah, that’s a great question. There’s a few different lenses, size of business and gender. Let’s take size of business. There’s two components. So one is the content needs to be tailored for the right size of business, but also the approach. So what Grow Your Business does is we begin the program with a diagnosis where the businesses take what we call the practices survey. And the survey aims to discover which practices are already being implemented and which aren’t. So it’s not how much do they know, it’s what are they doing. And based on that survey, the entrepreneur chooses five things that they want to implement in their business. So it could be starting to forecast that cash flow, starting to do one on one meetings with their direct reports. We’re not prescribing a learning journey. The entrepreneur decides what’s important for them. Now, that works really well for an entrepreneur who’s a little bit more established and who knows enough about their business to be able to identify what they need to do. What we’ve found is with earlier stage or smaller entrepreneurs, they need more direction and so they don’t yet know what they don’t know. And so they need a more directed learning journey. So that’s the big difference that smaller micro entrepreneurs need more guidance.

In terms of gender, we’ve seen some really interesting trends. So we noticed on the program with KCB, for example, at the intake level, there were, I believe, it’s 55 percent men and 45 percent women. When we looked at the completing entrepreneurs, that ratio had flipped. So 55 percent of the competing entrepreneurs were women and 45 percent were men. So women were more likely to complete the program. It seems based on qualitative feedback that they were more likely to translate what they’d learned into real impact for their business. So they were more likely to be implementing the practices, more likely to be growing their revenue, creating jobs.

Anna Gincherman [00:08:44] And why do you think that is?

Rebecca Harrison [00:08:46] Yeah, that’s the big question. We have a few hypotheses that haven’t been tested. We think that because there are potentially fewer opportunities available to women, that when they get an opportunity like this, they’re more likely to seize it for the reasons that, you know, you at CCX have documented, life is particularly challenging for a female business owner. And so, you know, when you get an opportunity, you seize it and you run with it. That’s one hypothesis. Another is that the blended learning approach may be particularly well-suited to women who might have multiple responsibilities. Instead of having to take a whole week out to come to class, they’re able to access learning on their phone in the evening during a break. And we’ve had feedback quite consistently from women that they really appreciate that flexibility.

Narration [00:09:35] Through AMI’s flexible schedule and innovative curriculum. Wanjiru finally got the motivation she needed to start her clothing business.

Wanjiru Mbugua [00:09:44] After the 2017 elections, my other business, the marketing PR business was really slow. And I was thinking, what other business can I come up with. Then a friend of mine told me about this KCB workshop that she had been invited to. So she invited me to go and I went. And after that workshop, we were invited to join a program that would take about six months. It was a pilot program, Grow Your Business, GYB. And so they said, if you’re ready, we would start in January and to finish in July. I said, why not? Because the schedule appeared to be reasonable, because it wasn’t every day like a compass or any other school program. And so it was going to work for me. I had this idea, but had not started, RD clothing. And so when we started on the second month of my training, I remember there’s this trainer who asked us “what do you think are your four best ideas, business ideas that you can work with from the comfort of your bed? ” You know. Something that people would be using, something that people would like, something unique, something interesting that you would do as a business and change your life and channge other people’s lives. I said “That’s it.” That’s it for me. That was it. That’s was all I needed.

Wanjiru gives a customer outfit ideas.

We’ve seen our NPS score go very high because of that extra mile that we have gone with the customers and it has also increased customer satisfaction levels to double-digit growth. So the non-financial services, comes as a pillar within the business model.

– NAOMI NDELE

Head of SME Banking, Kenya Commercial Bank

Rebecca Harrison [00:11:07] Another really interesting aspect of GYB is the peer to peer networking and mentoring. We definitely have program managers who are journeying with our entrepreneurs to help them extract insights and apply those to the business. But also where a lot of the learning happens, we believe is between the entrepreneurs themselves. There’s a lot of evidence to suggest that a) entrepreneurs love networking. I’ve never met an entrepreneur who does not like networking. And also, you know, being a business owner can be lonely. They really get a lot of value from engaging with other business owners and learning from them. We actually structure quite formally into the program what we call pods, which are small groups. In between the formal workshops and while they’re accessing tools on the online platform, they’re also meeting in small groups and they’re sharing what they’re learning and critically they’re holding each other accountable to what they’re learning. And with we’re discovering that a lot of the value seems to be coming out of these pod groups.

Narration [00:12:11] For Samuel, a private school entrepreneur based in Nairobi, the close bond of his pod outlived the duration of the program.

Samuel Njenga [00:12:19] We were also joined with other business people. We formed pod. That we could even meet without the trainer, discuss. And up today, we are still challenging each other, talking, communicating. So that has really helped me a lot.

Anna Gincherman [00:12:35] From what we know that the partnership with KCB Group in Kenya was one of the first of AMI’s partnership with a banking institution. And we see more and more leading banks try to expand their SME proposition, understanding that it’s not only about access to finance, but it’s also about access to knowledge, access to skills, existing network, and that can really facilitate that business growth of their clientele. So from your point of view, where do you see the kind of the benefit for banks of partnering with institutions for yours?

Rebecca Harrison [00:13:20] Yeah. Well, first of all, we loved working with KCB. They’re a great partner, really engaged and really invested in the success of that of their business club members, entrepreneurs. Yeah. I mean, for me, the key benefits for the bank are around de-risking of the businesses.

Narration[00:13:38] As the head of SME banking at KCB, Naomi Ndele pays close attention to the impact of non-financial service programs on clients and on the bank’s overall portfolio growth.

Naomi Ndele [00:13:51] We had customers whose loans were going to be called up, but from the lessons of this training, they were able to restructure their finances and pay up their loans and actually completed the repayment of the loan within that the year of the AMI program. So the benefits of the blended learning were really impactful to the customers, which also resulted in a benefit to the bank in the sense that we were able to recover loans that were almost going bad.

Rebecca Harrison [00:14:22] The second is just the power that it gives the brand, I think. I mean, when we worked with the KCB clients, we really saw them that the way that they felt towards KCB really turned around and shifted during the course of that program. So many of them saw such transformation and they saw KCB as an intrinsic part of that transformation and an intrinsic driver. So again, for the bank, having your brand associated with transformation in a business and the impact that’s going to have, I would imagine on a loyalty, client loyalty and kind of net promoter score would be really significant.

Naomi Ndele [00:15:01] We’ve seen our NPS score go very high because of that extra mile that we have gone with the customers and it has also increased customer satisfaction levels to double-digit growth. So the non-financial services, comes as a pillar within the business model. It goes beyond just giving products and solutions to walking the journey of building a business with a businessperson.

Samuel at his school in Nairobi, Kenya

Rebecca Harrison [00:15:35] The other kind of real differentiators of your business is that we’re razor-sharp focused on business impact. Most training programs, the only metric they track is bums on seats or number of people trained and they really don’t track in any kind of rigorous way the real impact on the business. For a lot of the traditional training programs in entrepreneurship around Africa, we don’t actually really know if they work. Not only do we take impact measurement really seriously, but we’ve actually embedded it into the core of the program. We believe that if you measure it, it gets done. A core part of this program is helping entrepreneurs see that if they understand what’s happening in their business, they can identify the core drivers and they can make good decisions. the first thing they do when they come on to grow your business is to start tracking their revenue, their costs, their profits. And we also ask them about the size of their workforce. So we can eventually track job creation and what we see immediately as once they start doing that, they suddenly realize are not quite making the amount of money that I thought I was. And that really quickly concentrates their minds. They get bought into the program really quickly because they start seeing where they can make more money, which is all entrepreneurs want to do. And they quickly start then using some of our tools to negotiate with suppliers to reduce their costs through minimizing waste. They stop serving their customers so they can see what their customers really want. How can they maximize revenue? They start changing the way they deal with their team and thinking about how they deal with their employees.

Samuel Njenga [00:17:10] One is how my staff are today. The way I deal with them, with the training that I got, they are very happy. We do a lot of team building. We do a lot of training and therefore they are really empowered. It is through them that I’m able to get the results that I’m getting in the classroom because I’m the manager. I’m not able to teach every child or even I don’t teach. I do the management. Therefore, by empowering my staff, by giving them a lot of exposure, doing a lot of team building, meeting their needs as they give the feedback, they do the work and therefore we get the results.

Rebecca Harrison [00:17:53] So you see that because they’re measuring what’s happening in the business, that’s what actually drives the impact. And then, you know, of course, it feeds itself. So then we go on to kind of measure business impact against those metrics on a regular basis during and beyond the program.

Narration [00:18:09] Since Anna sat down to talk with Rebecca in late January, AMI has had to make considerable changes to their delivery of educational material as a result of the public health implications of Covid-19. For the foreseeable future, all of AMI’s classes and session will be online. To retain the aspect of “human touch element,” AMI will be conducting webinars and video conferencing where participants will have the opportunity to role play and network with other members in their cohort. For businesses struggling to adjust to new financial burdens and changing work environments, AMI is now offering a free ‘Covid-19 virtual business survival bootcamp. Through this bootcamp, entrepreneurs can learn how to manage remote teams, lead in a crisis, optimize health and hygiene at work, and financial forecast in an economic slowdown.

In these uncertain times, the need for SMEs to learn, adapt and thrive is paramount for the global economy to rebound. Over the next few years, ConsumerCentriX looks forward to partnering with AMI on developing scalable solutions that will equip SMEs across Africa with the right practices and habits to grow their business and create economic stability for their families and communities.

To learn more about AMI's COVID-19 bootcamp click here

Anna and Rebecca after wrapping up the interview

MORE PODCASTS

Don't miss an episode of Reaching the Underserved.

Sign up for our newsletter.

Why 2019 Mattered for Us

A REFLECTION

Why 2019 Mattered for Us

As a company committed to closing the gap in financial access, 2019 was a monumental year for us. We are proud to have embarked on several key initiatives that have laid the foundation for our work in the years to come.

– CONSUMERCENTRIX LEADERSHIP TEAM

Identifying Practical Solutions for Regulators to Accelerate Financial Inclusion

In the summer of 2019, we convened key regulators from Nigeria, Egypt, and Indonesia to share lessons among peers and draw inspiration from digital and policy innovation in India, China and Estonia. The result? Roadmaps that gave new momentum to financial inclusion. We look forward to continuing our work with this dedicated group in 2020. Stay tuned for more details!

Click here to learn more about this study.

Insights into the business case for non-financial services to women-owned SMEs.

To help close the gap in financial access and knowledge, the International Finance Corporation (IFC) and the Netherlands Development Finance Company (FMO) enlisted our support to provide insights in the business case for non-financial services to women-owned SMEs. To get a holistic view of the state of non-financial service (NFS) offerings in 2019, we surveyed over 30 banks from around the world.

Through an in-depth analysis of survey data and interviews with key stakeholders from financial service providers, enterprise development organizations and other industry players, we gained actionable insights into new NFS delivery models and determined a tiered approach for financial service providers to improve their business outcomes by providing non-financial services to women-owned SMEs.

Keep an eye on our social channels and website. Because in 2020, we will publish our findings and insights through two case studies, blogs, and a podcast.

Working with East African Banks to address the complex needs of SMEs

Through the generous funding of the Argidius Foundation, we worked with two leading banks in East Africa, Stanbic Bank Uganda and KCB Rwanda to develop holistic SME Banking propositions with an emphasis on non-financial services. To determine the feasibility of the propositions, we assessed the financial, business skill, and networking needs of SME customers and non-customers and their attitudes towards financial institutions.

Convinced from the findings and business opportunities determined by the feasibility studies, the Argidius Foundation has extended its funding through a grant of 1.5 million euros. As a result of this funding, we will continue working with both banks, to address the complex needs of SMEs through financial and non-financial services over the next three years. By providing SMEs in Uganda and Rwanda with the right finance and skills to expand their businesses, both countries stand to benefit from catalyzed economic growth.

P.S If you haven’t listened to our new podcast series “Reaching the Underserved,” check out our first episode with Nicholas Colloff, Executive Director of the Argidius Foundation.

FROM THE NEWSROOM

Don't miss a new insight in 2020.

Sign up for our newsletter.

Understanding the Customer First

VALUE DNA

Understanding the Customer First

Through our consumer insights, we can effectively guide financial institutions and fast-moving consumer goods companies towards developing brands and products that resonate with customers. Watch the video to learn more.

Breaking Down Bias and Increasing Financial Access in Central Asia for Women-Led SMEs

Breaking Down Bias

and Increasing Financial Access in Central Asia for Women-Led SMEs

European Bank for Reconstruction and Development (EBRD) enlisted the services of ConsumerCentriX to conduct market assessments in Mongolia, Uzbekistan, and Kyrgyzstan. The findings determined key constraints faced by women-led SMEs when it came to accessing finance and recommendations on possible measures that would mitigate systemic barriers. In this video, Benedikt Wahler, Partner of ConsumerCentriX, discusses the role unconscious bias plays in constraining access to finance for women-led SMEs in all three countries.