Publication: Opportunities to Foster Digital Financial Services Market Development in Guatemala

Published in November 2023, the “Opportunities to Foster Digital Financial Services Market Development in Guatemala” report examines how digital financial services can better serve low-income and marginalized populations, particularly women, while supporting the responsible growth of Guatemala’s financial sector. The market assessment was funded by USAID through the Digital Frontiers program, implemented by DAI, and conducted by ConsumerCentriX Inclusive Business.

The study addresses persistent gaps in financial inclusion in Guatemala, where many low-income households primarily interact with formal financial institutions through over-the-counter transactions to cash out remittances or government payments. Despite expanding the digital infrastructure, the adoption of digital financial services remains limited, particularly among women, Indigenous communities, and rural populations.

Rather than taking a broad or purely diagnostic approach, the research focused on specific population segments where there was a balance between potential impact and realistic readiness for digital uptake. These included international and domestic remittance recipients, domestic workers, and rural agricultural MSME retailers. The assessment combined qualitative fieldwork, stakeholder interviews, and prototype testing to examine financial behaviors, cash-flow patterns, and barriers to adoption from the customer perspective.

The findings challenge common assumptions held by financial service providers. While low literacy and lack of confidence are often cited as primary barriers, the research shows that trust, opaque fees, limited product relevance, lack of formal identification, and weak customer experience play a more decisive role. Participants across segments demonstrated regular income flows, access to smartphones, and openness to using digital tools when they deliver clear and tangible value.

The report highlights the importance of entry products linked to existing cash flows, such as remittances, salaries, and government payments, combined with high-touch on-boarding and customer education. It also highlights the role of regulation, national ID coverage, and coordination between public and private sector actors in enabling inclusive and sustainable digital financial markets.

Learn more from the report: Opportunities to Foster Digital Financial Services Market Development in Guatemala

ConsumerCentriX Participates in Sensitization Workshop for WE Finance Code In Uganda

Ugandan stakeholders have taken a bold step in their journey to become a signatory of the Women Entrepreneurs Finance Code (WE Finance Code), by convening a sensitization workshop that brought together 26 Commercial Banks, 35 Micro Finance Institutions (MFIs), representatives from the Central Bank – Bank of Uganda (BOU), representatives from the country’s Parliament, the FinTech Association and representatives from development partner institutions, to understand what the Code is, and the nature of commitment required for national champions and coalition partners to pledge to increasing access to capital for Women Small and Medium Enterprises (WSMEs).

The meeting was convened by the World Bank Funded GROW Project, alongside the Ministry of Gender, Labor and Social Development (MOGLSD), Private Sector Foundation Uganda (PSFU), Bank of Uganda (BOU), Uganda Bankers Association (UBA) and Association of Microfinance Institutions in Uganda (AMFIU).

ConsumerCentriX facilitated the technical discussions that are central to the code, including The Strategic and Business Case for Serving WMSMES, Benefits of implementing the WE Finance Code Initiative In Uganda, and the Critical importance of sex-disaggregated SME data – a central element of the code and its implementation.

Stakeholders made a commitment toward actions that will enable Uganda join over 31 countries around the world that have already signed the code, including Rwanda, Tanzania, and Kenya, within the East African region. Stakeholders recognized the vital role WSMEs play in driving business growth, job creation, and economic development, and the challenge around insufficient collection, quality, and use of sex disaggregated data that plays a major role in sustaining the gender gap in financial services and access to capital for WSMEs.

“The first barrier [to access to capital] for women is poverty…” Minister of Gender, Labor and Social Development, Hon. Amongi Betty Ongom remarked and committed that her Ministry will support the We-Fi Code initiative as this will cause a shift in financial policies that increase access to capital for women. The Uganda Bankers’ Association (UBA) committed to championing the Women Entrepreneurs Finance Code (WE-Fi Code) in Uganda, as it is aligned with their Women Economic Empowerment Initiative (WEEI), that aims to position its member institutions as leaders in supporting women entrepreneurs and to drive data-driven decisions that improve financial services for WMSMEs.

The Association of Micro Finance Institutions in Uganda (AMFIU) also committed to championing the Code by ensuring it is fully integrated within SACCOs, MFIs, and other financial institutions across Uganda through leveraging their national network to turn the Code into a living instrument that unlocks finance, growth, and dignity for millions of women entrepreneurs who are the backbone of Uganda’s economy. The Bank of Uganda (BOU) highlighted their current investment in big data initiatives that directly align with the Code’s emphasis on data – not only to support evidence-based policymaking and regulatory oversight but also enable financial institutions to design products that better meet the needs of women entrepreneurs. The Bank of Uganda committed to working with all partners to translate the WE-Fi Code into measurable action, unlocking finance, driving innovation, and accelerating inclusive growth. The meeting gained consensus on what it will take for Uganda to launch the code, with commitments from key coalition and partner institutions emphasizing the collaborative efforts required through public and private partnerships. ConsumerCentriX is supporting Uganda’s implementation of the code.

WSME Segmentation Report, Framework And Toolkit

This Toolkit, which accompanies the Women-owned/led Small and Medium Enterprise(WSME) Segmentation Report, provides a step-by-step guide, enabling local financial intermediaries to develop customized lending and financial products that align with the specific needs of each WSME segment, funders to assess risk and allocate funding to support high-potential WSMEs, and business support organizations (BSOs) to design tailored programs that address challenges specific to each segment. This practical resource includes guides and downloadable tools across six robust steps: to scan the enabling environment surrounding WSMEs, conduct WSME customer segmentation and market analysis, assess the demand among WSMEs for financial and non-financial services, design financial and non-financial products and services, and quantify the market opportunity and business case.

ACCESS THE REPORT BELOW

ConsumerCentriX attends Nigeria's 2024 International Financial Inclusion Conference.

ConsumerCentriX participated in Nigeria’s 2024 International Financial Inclusion Conference (#IFIC2024), organized by the Central Bank of Nigeria, which took place on November 12-13 at the Landmark Event Centre in Lagos. This year’s conference theme, “Inclusive Growth: Harnessing Financial Inclusion for Economic Development,” brought together over 2,000 participants from 78 countries, including global thought leaders, industry practitioners, and influential stakeholders

The conference agenda featured dynamic plenaries, roundtables, and exhibitions showcasing innovations that advance financial access and address critical topics such as gender-inclusive finance, MSME financing, and digital financial solutions.

As a key contributor to the event, Anna Gincherman, Partner at ConsumerCentriX, spoke in the session “Powering Nigeria’s Inclusive Growth through MSMEs.” Drawing on ConsumerCentriX’s global expertise, Anna highlighted the importance of leveraging data to build effective financial solutions for micro, small, and medium-sized enterprises (MSMEs), focusing on women-led businesses.

Beyond Anna’s session, ConsumerCentriX celebrated significant milestones during the week:

- Launching the Women’s Financial Inclusion Dashboard: Together with the Central Bank of Nigeria and the Nigeria Inter-Bank Settlement System PLC (NIBSS), ConsumerCentriX unveiled the Women’s Financial Inclusion Dashboard. This innovative data portal offers granular, up-to-date information on access and usage of financial services in Nigeria. Work is now underway to expand the portal with sex-disaggregated SME data, expected by the end of November. Visit the dashboard at www.wfid.ng.

- Onboarding Signatories to the WE Finance Code: Following the launch of the Women Entrepreneurs Finance Code (WE Finance Code), ConsumerCentriX, in collaboration with the Central Bank of Nigeria and the World Bank, co-led a workshop to onboard more than 30 signatories of the WE Finance Code, including 12 leading banks. This initiative emphasized the responsibilities and benefits of joining the Code, including capacity-building opportunities and peer learning programs presented by the Financial Alliance for Women.

- Collaborative Dialogues: ConsumerCentriX contributed to rich discussions during #IFIC2024, sharing insights on leveraging data to create impactful SME solutions. The event provided an opportunity to reconnect with colleagues and industry pioneers who continue to drive digital financial inclusion and innovation in Nigeria.

ConsumerCentriX is committed to fostering inclusive growth and supporting initiatives empowering MSMEs and underserved segments including, WMSMEs globally.

Developing a Global Segmentation Framework and Toolkit for Women-Led/Owned SMEs.

Facilitating greater capital flow to women-led businesses is crucial for fostering economic growth and empowerment. Despite increasing awareness of the gaps women SMEs (WSMEs) face in access to capital and banking, the supply-side response has not been intentional in targeting segments of WSMEs with unique products and services and altering their processes to serve them better. While the social and economic benefits are clear, policy and private sector priorities have not consistently aligned around supporting WSMEs in an effective manner. ConsumerCentriX, with the support of the Women Entrepreneurs Finance Initiative (We-Fi), Argidius Foundation, and the Dutch Good Growth Fund (Triple Jump), is developing a WSME Segmentation Framework and Toolkit to address this gap. The framework and toolkit aim to transform how financial sector stakeholders understand and serve women entrepreneurs and business owners.

Current market segmentation practices for WSMEs are largely supply-driven, focusing primarily on business size and gender split. This narrow approach of segmenting SME markets by business size and overlaying a definition of women enterprises fails to address the critical dimensions that define her and her business. Financial sector stakeholders need a nuanced segmentation to tailor their support and services in a way that effectively supports different profiles of WSMEs to grow.

Based on primary findings from literature reviews and stakeholder interviews conducted in phase one of the project, it became evident that existing frameworks are insufficient at addressing the unique circumstances of women SMEs. While some frameworks include personal and psychological dimensions, none offer a comprehensive view that provides for critical factors like household responsibilities and dependents. This highlighted the need for a new, holistic approach that considers the full spectrum of influences on women entrepreneurs, including the environment in which she operate and how supportive or restrictive elements like social and gender norms and legislation are.

The WSME Segmentation Framework and Toolkit developed through this project leverages a gender-inclusive approach to segmenting WSMEs: by beginning with her as an entrepreneur or business owner, separating her from her business, and placing her and her business in the environment where she operates. These factors determine the growth path that her business is on, whether low/no growth, steady growth, or high growth/venture.

Through quantitative and qualitative research with WSMEs in Pakistan, Uganda, and Colombia, CCX will be able to determine which factors about her as a person, her business and the enabling environment are deemed the strongest determinants of which growth path she ends up on. From there, CCX will define segments and profiles using the factors. Marrying that insight with learnings from research on the supply-side, the final Global Segmentation Framework will illustrate not only the descriptors/dynamics and financial/non-financial needs per segment but also the supply-side response to target each segment and where the gaps are.

Ultimately, the goal of the WSME Global Segmentation Framework and Toolkit is to provide financial sector stakeholders with the tools and insights needed to offer more targeted and practical support to women entrepreneurs.

Strategies for Financial Service Providers to Access Colombia's Untapped MSME Market

Author: Laura Trueba, Head of Latin America and the Caribbean

Co-author: Musa Kacheche, Corporate Communications Lead

Date: June 28th, 2024

Area Covered: Latin America and the Caribbean

Topics:

MSME Banking • Financial Inclusion • MSME Research • Market Segmentation

The Current State of MSME Banking

Micro, small, and medium-sized enterprises (MSMEs) are crucial to the economic fabric of Latin America and the Caribbean. In Colombia, they account for 99% of companies, 80% of private employment, and 35% of GDP. Despite their significance, MSMEs in Colombia remain underserved. They receive only 14% of total commercial loans, facing a financing gap estimated at $56.2 billion—19% of the 2017 GDP—for formal MSMEs alone. Informal companies face an additional financing gap of 10% of GDP, while women-owned MSMEs experience a shortfall of $6.1 billion.

Addressing this gap requires continued efforts by the government and financial institutions to develop innovative solutions that meet the unique needs of MSMEs in the Colombian market. With funding from the Argidius Foundation, ConsumerCentriX conducted a market feasibility study to identify barriers to access finance for MSMEs in Colombia. The study involved customer research engaging business owners in Bogota and Medellin and a market analysis involving interviews with key industry stakeholders, such as financial service providers (FSPs), government institutions and other MSME ecosystem partners.

Understanding Customer Perspectives

Despite a dynamic MSME sector with over 5.7 million enterprises, Colombia’s 1.4 million registered micro-enterprises face a vast gap in accessing financial services. These businesses often rely on retail banking solutions rather than tailored business products. For instance, they often opt for personal loans over business loans due to stricter requirements, lengthy approval processes, and high fees associated with the latter. While personal loans are more accessible, they often come with higher interest rates and rigid repayment terms, which do not align with the financial needs of the businesses. Additionally, most entrepreneurs are unaware of the offerings from the largest banks, and those familiar with them find the products unsuitable. Colombia’s registered microenterprises tend to be “multi-banked,” meaning they use financial services from different institutions, seeking the most favorable options. For example, they may take out personal loans, open deposit accounts, or access business credit from various banks. As a result, these businesses do not depend on comprehensive solutions from a single FSP but diversify their services across multiple providers.

Moreover, MSMEs in Colombia value having a dedicated point of contact at their bank, such as a relationship manager who understands their business and can offer personalized advice. The availability of knowledgeable financial advisors or loan officers helps MSMEs make complex financial decisions and grow their businesses. Furthermore, MSME owners expressed a need for non-financial services, such as business training and access to networks, to support their growth. Many business owners whose educational backgrounds may not prepare them for a growing business seek opportunities to develop essential skills and knowledge. Colombia has a diverse ecosystem of MSME support institutions, but the fragmented landscape makes it difficult for business owners to know where to access these resources.

Understanding the Competitor Landscape

Market analysis reveals intense competition in the small and medium enterprises (SME) banking sector, where major banks offer tailored and holistic market solutions. A similar level of competition exists among microfinance institutions serving the unregistered micro-enterprises. However, a significant opportunity exists within the registered micro-enterprises segment, which remains largely underserved by financial service providers.

Despite the evident need for financing among registered micro-enterprises, banks remain cautious due to perceived credit risks. Most financial institutions prefer lending to well-organized SMEs, focusing on legal entities and secured loans backed by government programs like the National Guarantee Fund (FNG), mortgages, or leasing programs. For microfinance institutions, the challenge is adapting their models—both in terms of human resources and product portfolios—to meet the needs of formal businesses. Offering lower-cost financing and overcoming the challenge of building brand recognition are additional obstacles in this space.

To differentiate themselves, FSPs should offer financing solutions that help registered micro-businesses achieve short- and long-term goals, such as purchasing machinery, expanding locations, acquiring raw materials, or maintaining cash flow with suppliers. These businesses expect low interest rates, simple requirements, fast approval, and transparent information. They also desire flexible repayment options and personal guidance from advisors who can explain the products and recommend the best options.

In conclusion, Colombia’s financial service sector holds significant potential for serving the registered micro-enterprise segment. By partnering with business development service providers and other key ecosystem players to bridge the skills gap, FSPs can position themselves as critical enablers of the growth and development of this segment in Colombia.

ConsumerCentriX Participates in and Co-organizes Two-Day Workshop on WE Finance Code in Georgia

ConsumerCentriX (CCX) had the privilege of co-organizing a two-day workshop in partnership with the European Bank for Reconstruction and Development (EBRD) and the National Bank of Georgia (NBG). The workshop focused on advancing financial inclusion for women-led enterprises in Georgia, an important step towards improving access to finance for Women-Owned Small and Medium Enterprises (WSMEs).

Day 1: Leveraging Data for Advancing Finance to Women Entrepreneurs

The first day began with a comprehensive analysis of Georgia’s WSME Finance Landscape. High-level representatives from the private sector and key ecosystem stakeholders attended the session, which opened with welcoming remarks by Ms. Natia Turnava, Acting Governor of NBG, and Mr. Alkis Vryenios Drakinos, Regional Head of Caucasus at EBRD.

Anna Gincherman from CCX set the stage by providing an insightful overview of international developments in gender-disaggregated data. She highlighted the business case for collecting and analyzing this data, revealing that while women-owned enterprises constitute around 32% of all SMEs in Georgia, they account for only 7.5% of formal credit access. This gap underscores the importance of developing targeted financial solutions for women entrepreneurs.

David Taylor of CCX followed by introducing the WSME Dashboard (https://www.wefinancegeorgia.ge/), an analytical and data visualization tool designed to provide insights into the financial landscape for WSMEs. The Dashboard sparked lively discussions among participants, who explored its potential applications for their own institutions.

Later in the day, Ms. Aurica Balmus, Principal of Gender and Economic Inclusion at EBRD, gave an in-depth presentation on the WE Finance Code and its potential impact on Georgia’s financial sector, particularly in improving access to finance for women-led businesses.

The session concluded with a presentation by Mr. David Utiashvili, Head of the Financial Stability Department at NBG. Mr. Utiashvili shared the regulator’s vision for the future of the WSME Dashboard, calling for collaboration between financial service providers (FSPs) and other stakeholders to enhance its capabilities. His remarks emphasized the need for collective efforts to ensure that the Dashboard becomes a valuable tool for increasing financial inclusion for WSMEs in Georgia.

Day 2: WE Finance Code – Data-Driven Strategies for Financing Women-Led Enterprises

The second day took a more interactive approach, with participants from financial institutions, including data, product, and ESG managers, as well as representatives from the Georgian Bankers Association. The discussion centered on their experiences working with the WSME segment and sex-disaggregated data.

Istvan Szepesy and Anna Gincherman from CCX led the morning session, focusing on strategies for capturing and managing gender data. They encouraged participants to critically assess their current data collection and analysis methods and offered practical recommendations for improvement.

David Taylor returned to share emerging insights from the WSME Dashboard, illustrating how the tool can inform data-driven decisions for financial service providers. Participants actively engaged in discussions on how the Dashboard can be further integrated into their day-to-day operations.

The workshop concluded with a presentation by Ms. Dana Kupova, Head of Inclusive Finance at EBRD, who outlined how EBRD could support banks in Georgia as they work to better serve women-led enterprises. Her remarks highlighted the growing opportunities for financial institutions to create tailored products and services that address the unique needs of WSMEs.

Looking Ahead

The two-day workshop demonstrated the power of collaboration between public and private sector stakeholders in advancing financial inclusion for women-led businesses. It also underscored the importance of data-driven strategies in fostering sustainable growth and access to finance for WSMEs.

We extend our heartfelt thanks to all participants for their active involvement and to the National Bank of Georgia, especially Salome Tvalodze and David Utiashvili, for their ongoing support and collaboration in developing the WSME Dashboard and organizing this impactful event.

As part of the ongoing implementation of the WE Finance Code in Georgia, CCX, EBRD, and NBG remain committed to working together to enhance financial access for women-led MSMEs and support their continued growth and success.

Press Release: Workshop on WE Finance Code

Examining Key Financial Inclusion Barriers in the LAC Region through ConsumerCentriX's Ecosystem-Centric Engagements

Author:

Laura Trueba, Head of Latin America and the Caribbean

Date:

June 28th, 2024

Area Covered:

Latin America and the Caribbean

Topics:

Financial Inclusion • Women’s Financial Inclusion • Gender-Inclusive Finance• Financial Regulation • Digital Financial Services

In the past two years, ConsumerCentriX (CCX) has undertaken important projects aimed at addressing barriers to financial inclusion in the Latin America and Caribbean (LAC) region. Drawing upon years of experience and more recent engagements, which included collaboration with Multilateral Development Banks (MDB), regulators and financial service providers (FSPs), CCX has an ecosystem-centric understanding of the financial inclusion landscape in the region. This approach has allowed us to identify and address the major challenges hindering greater financial inclusion in the region. To shed light on these major challenges, this blog will highlight some significant barriers.

Among the interventions that have empowered CCX to gain this valuable understanding include the Supply-side Sex-disaggregated Data Survey, commissioned by IDB Invest, reaching 13 LAC countries. This survey covered over 240 financial service providers in the region to understand their strategies for the women’s market, including mapping their financial and non-financial product offerings and their use of sex-disaggregated data. This resulted in a publication, “Women Rising“, highlighting, among many other insights, the untapped revenue potential in the women’s market, ranging from $1.87 billion in Mexico to $283 million in Guatemala.

Regarding the state of financial inclusion of women micro, small and medium businesses (WMSME), CCX has been recruited by IDB Invest to support the successful implementation of the Women Entrepreneur Finance Code (We-Fi Code) in the Dominican Republic. This will involve enhancing the capacity of the Asociación de Bancos Múltiples (ABA) as the local Aggregator and Coordinator, as well as FSPs, to fulfil the commitments of the Code.

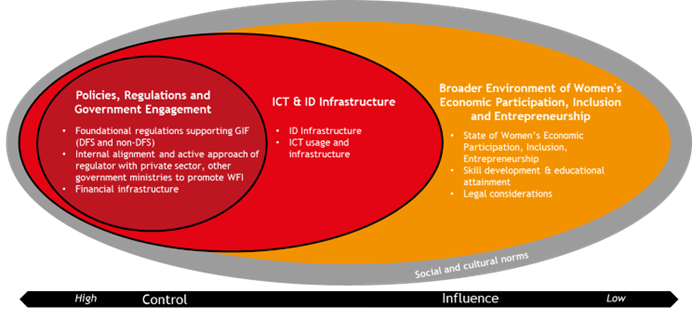

On the regulatory side, CCX collaborated with the Alliance for Financial Inclusion (AFI) to develop a Gender-Inclusive Finance (GIF) Roadmap for AFI 11 member countries in the LAC region. This initiative aimed to systematically review practical policy actions to enhance women’s financial inclusion and reduce gender gaps. CCX also worked with AFI to conduct case studies of 13 countries, including eight from the LAC region, to understand the role regulators play in closing the financial inclusion gender gap.

To conduct these case studies, an Analytical Framework for Inclusive Finance with a Gender Perspective was developed in partnership with AFI that comprises four key spheres that impact the state of financial inclusion in a country, such as 1) FSP’s actions towards women’s financial inclusion, 2) Policies, Regulations, and Government Engagement, 3) ICT and ID Infrastructure, and 4) the Broader Environment of Women’s Economic Participation, Inclusion, and Entrepreneurship.

Unveiling Financial Inclusion Disparities Between Rapidly Progressing and Slower Progressing Countries

- Delving into the regulatory landscape

Following our assessments and employing the AFI Framework for Inclusive Finance with a Gender Perspective as the analytical cornerstone, a significant disparity is observed between countries with limited financial inclusion and those that have made substantial progress. This disparity primarily revolves around the availability of financial infrastructure, the network of banking agents, their outreach, and utilization, which must also include mobile money/digital solutions services. Some developed regulations lack a digital financial services component, particularly concerning the interoperability of mobile banking, primarily within banking agents.

Interoperability, Open Banking, and National Financial Inclusion Policy in Perú

The Central Reserve Bank of Perú (BCRP) has been working on increasing interoperability to promote digital payments and financial technology and further drive financial inclusion. As of 2021, 44% of women and 55% of men reported making or receiving a digital payment to Global Findex, which is high for the region. To support the prevalence of digital payments, the BCRP has worked to strengthen retail interoperability, especially since the COVID-19 Pandemic. Today, over 100,000 retailers across the country are compatible with e-money. The BCRP has stated that payment providers must be interoperable, setting an implementation schedule for interoperability. The BCRP also runs the payment switch for interbank transfers, checks, ATMs, and mobile money, all integrated under the real-time gross settlement system.

Furthermore, we have observed that alongside mobile interoperability, there is a crucial need to ensure adequate regulation of mobile and digital financial services. Such regulation should permit electronic wallets for retail payments, facilitate the opening of e-wallets without mandatory linkage to a bank account, and enable digital customer identification (e-KYC) for individuals to open e-wallets or basic bank accounts remotely.

E-Wallets in El Salvador

E-wallets in El Salvador are driving financial inclusion, with uptake that is outpacing that of traditional bank accounts. In 2015, the country passed the Law to Facilitate Financial Inclusion; while the law spans many areas including tiered KYC, arguably its most important provision is the regulation of e-wallet providers and savings accounts with simplified requirements. The law imposes disclosure requirements, consumer protection standards, provides transaction limits for agent banking, and authorizes banks to issue their own mobile money services.

By paving the way for e-money and its use in the country, the law resulted in explosive growth of the MNO Millcom’s Tigo Money. Today, over 1 million Tigo Money accounts exist in El Salvador, representing about 20 percent of the adult population, which is immense compared to the 29% of women and 45% of men who own a bank account according to Findex 2021.[1]

More recently, in 2021, El Salvador’s government passed the Bitcoin Law and the roll-out of Chivo, a government-owned e-wallet for cryptocurrency and dollars. As of 2021, 3 million Salvadorians have downloaded the app and created an account, amounting to 46% of the population, 52 percent of which are women.

- Delving into the financial service provider landscape

According to the IDB Invest Supply-side Sex-disaggregated Data Research Survey, most FSPs in the region focus on the women’s market but still consider it part of their corporate social responsibility strategy. There is a clear knowledge gap on the business case and profitability of serving the women’s market, attributed to a lack of capacity to collect, use and analyze sex-disaggregated data. Moreover, without this data, FSPs are unable to develop holistic women’s market strategies, which are crucial for designing and marketing offers and products aimed at women clients.

While 75% of commercial banks in the region reported collecting sex-disaggregated data, over half (52%) continue to use manual reporting processes, which raises concerns about data quality, and most still have not established key performance indicators (KPIs). Furthermore, FSPs with advanced market strategies generally do not leverage the available data to evaluate return on investment or profitability.

As a result, they overlook clear business expansion opportunities, given their lack of emphasis on profitability as a reason for targeting the women’s market. By not thoroughly analyzing their existing data, FSPs may be missing a crucial business strategy for enhancing their focus on women.

Addressing financial inclusion barriers in the LAC region is crucial for socio-economic development. This requires collaborative efforts from regulators, FSPs, public entities, civil society organizations, and development partners. By continuing to innovate and adapt, CCX is paving the way for a more financially inclusive future.

Empowering Women Entrepreneurs in Sub-Saharan Africa through the Africa Women Rising Initiative

Author:

Benedikt Wahler, partner

Date:

June 26th, 2024

Area Covered:

Africa, Sub-Saharan Africa

Topics:

Financial Inclusion • Women’s Financial Inclusion • Micro, Small and Medium Enterprises (MSMEs) • Financial Regulation • Research

For the last four years, ConsumerCentriX, in collaboration with the International Project Consult (IPC) and the African Management Institute, has supported the implementation of the Africa Women Rising Initiative (AWRI), funded by the European Investment Bank (EIB). In mid-June, Benedikt Wahler and Dörte Weidig, partners at ConsumerCentriX and IPC, respectively, delivered a “Knowledge Lab” session in Luxembourg to the EIB community to share the large-scale impacts and lessons from this work.

This initiative aims to empower women economically in Sub-Saharan Africa by increasing their access to finance and capacity-building resources, particularly for women entrepreneurs, owners, and leaders in micro, small, and medium enterprises (MSMEs), in alignment with the 2X Challenge criteria.

AWRI Pilots and Builds a Foundation for Mobilizing Large-Scale Gender Finance

As part of the broader “SheInvest” initiative, through which the EIB is mobilizing EUR 2 billion of funding for gender-responsive investments in Africa, AWRI was launched in April 2020. This occurred just as Africa was experiencing the first wave of the COVID-19 pandemic to complement these funds with technical assistance (TA) from the consortium partners.

From the ConsumerCentriX team and our professional network, we contributed the Team Lead, interim team lead, and several senior experts on key factors for the success of gender-inclusive finance: unsecured and cashflow-based lending, market research, strategy and value proposition design, as well as facilitating the work of cross-functional teams to pilot new approaches. Our data team also helped ensure the recommendations reflected a sound basis of analysis and insights.

ConsumerCentriX Managing Director Benedikt Wahler, who stepped up from key expert to interim Team Lead during a medical leave, feels that “AWRI really showed once more the full breadth of expertise we were able to mobilize and the deep bench of colleagues to make one more multi-year, multi-country, and multi-institution TA a success.” It was another instance of a close and successful collaboration with IPC, alongside current joint activities on “Youth-in-Business” and the upcoming Central Asia WE Finance Code.

Thanks to AWRI, nine financial intermediaries (FIs) across four countries – Uganda, Rwanda, Senegal, and Côte d’Ivoire – received customized assistance based on a thorough assessment of their needs, the realities of their clients, and their local market context. In addition to four commercial banks (Bank of Kigali, Ecobank Group, Housing Finance Bank, Atlantic Business International), four microfinance institutions (Pride Microfinance, Centenary Bank, Baobab Senegal, Baobab Côte d’Ivoire), and one development bank (Development Bank of Rwanda) were supported on gender finance.

Before this work started, ConsumerCentriX pioneered a data-driven approach to identifying the right countries for gender finance interventions like AWRI. Using a proprietary benchmarking tool that considers four main dimensions of women’s economic, social, and financial inclusion, we screened and scored 45 economies in Sub-Saharan Africa.

The implementation focused on two main components: “Banking on Change” and “Market Maker.” “Banking on Change” targeted the supply side by enhancing the capability of financial institutions to meet the needs of women entrepreneurs with gender-intelligent products and services, while “Market Maker” focused on the demand side, strengthening women entrepreneurs’ financial and business skills and their networks.

Through the Market Maker initiative, AWRI significantly enhanced women entrepreneurs’ financial literacy and business management skills. Training programs reached 1,087 women, covering essential topics such as financial literacy, record-keeping, customer service, and soft skills. Forty per cent of the participating businesswomen subsequently obtained loans. This initiative also developed 11 non-financial services (NFS) modules tailored to the needs of women entrepreneurs, further supporting their business growth and sustainability. The impact of these efforts was evident, with many women reporting improved business practices and enhanced financial management skills.

The AWRI’s Banking on Change component focused on strengthening the capabilities of partner financial institutions (PFIs) to better serve women entrepreneurs. This included conducting comprehensive institutional diagnostics and capacity needs assessments, followed by tailored technical assistance packages delivered by a team of international and local experts. At two institutions, unsecured loan products and the respective credit processes were developed for the first time. Two others deployed their first-ever savings products tailored to businesswomen, leading to strong growth in their funding base.

Even though most improved solutions were still in the early stages of roll-out, the results were strongly positive. The number and volume of loans grew faster for women than men at all institutions. The portfolios now include 35,400 more women borrowers and EUR 67 million. Compared to the pre-AWRI baseline, our team helped advance the frontiers of inclusion: 16,000 women borrowers who otherwise would not have been expected to receive loans and EUR 40 million in loan volume. All of this was achieved while not merely preserving but even expanding the better repayment performance of women borrowers.

Why Gender Finance is the Right Approach for Impact and Commercial Success

The 2X Collaborative, of which EIB is a founding member, documents the growing momentum among the community of development finance institutions and related stakeholders that a dedicated focus on women (also known as a Gender Lens) delivers better impact. The evidence collected over the past decade by programs like the IFC’s “Banking on Women” or the Financial Alliance for Women from pioneering banks, MFIs, and fintechs around the world makes it clear that there is also a strong strategic and business case for targeting women and women SMEs as clients. At ConsumerCentriX, this reality and our expertise on what that should mean in practice drive around two-thirds of our work.

For those who care about impact, the case for being intentional in focusing on women should be straightforward: though women and men are diverse among themselves, on the criteria that matter for their ability to access and use conventional financial services, women score lower on average.

In the regional context of AWRI in Sub-Saharan Africa, women entrepreneurs face numerous challenges in operating and growing their businesses: less revenue and often smaller businesses in low-margin sectors, lower levels of secondary education and less professional experience in the formal sector, less likely to have mentors, and more limited access to capacity building, supportive networks, and market information. They are also often far less able to post the kind of assets required as collateral to obtain loans.

To truly deliver on the ambition of building an inclusive financial system that can power sustainable and broad-based economic growth, solutions ought to be benchmarked against the realities of such women – in other words, be “gender-intelligent.” To genuinely aim for reaching the marginalized parts among women and other groups, those experiencing the highest levels of such challenges should set the tone, thereby aiming for solutions that stand a chance of being “gender-transformative,” i.e., over time, wearing down these challenges rather than just working around them. The reality of supposedly fair “gender-neutral” approaches is that they are bound to fall short of most women and even a good portion of male users of financial services. They are designed for a type of client who is just not representative of the population at large – let alone those at the frontier of the financial system. (see charts below)

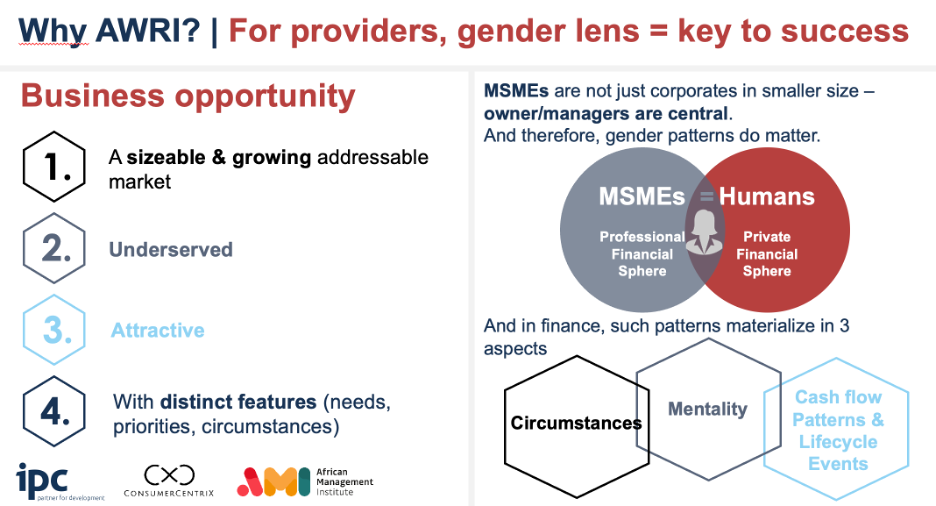

In the AWRI program – as in most of our work – we were tasked with working with for-profit financial service providers. There is now a strong basis of evidence that women and women’s businesses constitute a clear business opportunity. But business bankers tend to ask why they’d need to become “gender-intelligent” in their work. Is not a business and a leasing contract a leasing contract, whoever sits on the client side of the relationship?

For the ConsumerCentriX team, the answer is clear: to actually seize that opportunity, bank executives do well to look closer and remind themselves that what sets MSMEs apart is not that they’re smaller than big firms. It’s the human(s) at the heart of these businesses. The owners and managers whose ambitions, outlook, and idiosyncrasies shape what the business will end up doing – and this is why gender patterns matter. In the space of finance, such patterns emerge 1) from the legal, family, and socio-cultural circumstances in which women have to operate, 2) the mentality and attitudes they bring to financial questions, and 3) the way in which their cashflows are (much more strongly) exposed to lifecycle events like marriage, childbirth, divorce, or care for elderly parents. (see below)

Notably, the success stories featured at events like the Financial Alliance for Women’s Annual Summit come from institutions that have taken such insights into action. This year’s edition in London included two Champions, Access Bank Group from Nigeria and Kenya Commercial Bank, who referred to business banking solutions that emerged from their work with our own Anna Gincherman and Benedikt Wahler.

As Benedikt summed it up: “With the now concluded AWRI program, our team is proud to have laid excellent foundations for seeing more such pioneering examples scale up in Africa.”

Implementation of Women Entrepreneurs Finance Code in the Dominican Republic.

In the Dominican Republic, micro, small, and medium-sized enterprises (MSMEs) play a significant role in economic growth and employment rates, comprising 99% of all businesses and generating over half of the country’s jobs. Despite this, MSMEs face disparities in accessing financial services and resources. In particular, female-owned micro, small, and medium-sized enterprises (WMSMEs) struggle to access the needed services.

To address this, The Superintendent of Banks (SBDR) has mandated Financial Service Providers (FSPs) to collect and report sex-disaggregated data for individuals and commercial businesses. SBDR has partnered with other public institutions to align on the segmentation of businesses and, as a result, published the country’s first MSME dashboard in 2024, allowing them to enhance their understanding of credit offered to different MSME segments and identify gender gaps in access. However, challenges persist in collecting quality data and a standardized definition of WMSMEs. Findings from the IDB Invest and ConsumerCentriX Study revealed that 62% of banks collect sex-disaggregated, with 50% registering WSME data for their product offerings, indicating a need for further improvement in data collection practices.

Recognizing the necessity to address these challenges, IDB Invest, the private sector window of the Inter-American Development Bank Group, recruited ConsumerCentriX and the Financial Alliance for Women (FAFW) for the implementation of the Women Entrepreneurs Finance Code in the Dominican Republic. This pilot is private-sector led, which means that through key private sector partners, including the Banking Association and key FSPs, the project has the aim of reaching an industry-wide capacity to both disaggregate data by sex, and improve financial services for women entrepreneurs.

The WE Finance Code or the Code is a commitment by FSPs, regulators, and other financial ecosystem stakeholders to work together to increase funding and support to women-led micro, small, and medium entrepreneurs. The project is a timely initiative since the Code has already gained much-needed momentum following its successful launch at the FAFW Summit in November 2023, where key stakeholders in the country’s financial sector, including regulators, associations and FSPs, committed to the Code by signing the letter of intent.

The project involves building the capacity of the national coalition consisting of the local aggregator and coordinator of the Code, Bankers Association “Asociación de Bancos Múltiples de la República Dominicana” (ABA) and FSPs to execute the Code commitments. This will be achieved by supporting ABA in aggregating, analyzing, and visualizing the collected WMSME data, as well as supporting FSPs in collecting quality data on WMMSEs and using it to develop holistic propositions tailored to addressing the needs of women entrepreneurs.

The initial signatories to the Code include multiple banks such as BHD, Popular, Banreservas, Caribe, Scotiabank, Banesco, JMMB Bank, LAFISE, Promerica, Santa Cruz, Vimenca, and ADEMI, along with savings and credit banks like ADOPEM and Confisa. Also participating from the government sector in this initiative are the Central Bank, the Superintendency of Banks, and the Ministry of Industry, Commerce, and MSMEs. These entities play significant roles in the crucial aspects of the project’s execution and regulation.

The Code in the Dominican Republic is a pioneering initiative at the regional level that will establish guidelines for implementation in other countries on the continent. The project seeks to position the Dominican Republic as a model for other countries by documenting best practices through case studies and creating tools for other nations to learn from and develop their Codes.